The "Iceberg" Reality: 5 Costs That Surprise Almost Every First-Time Home Buyer

Saving for a down payment is a massive achievement. It takes discipline and sacrifice. When many first-time buyers finally hit that savings goal, they feel ready to jump into the market.

Saving for a down payment is a massive achievement. It takes discipline and sacrifice. When many first-time buyers finally hit that savings goal, they feel ready to jump into the market.

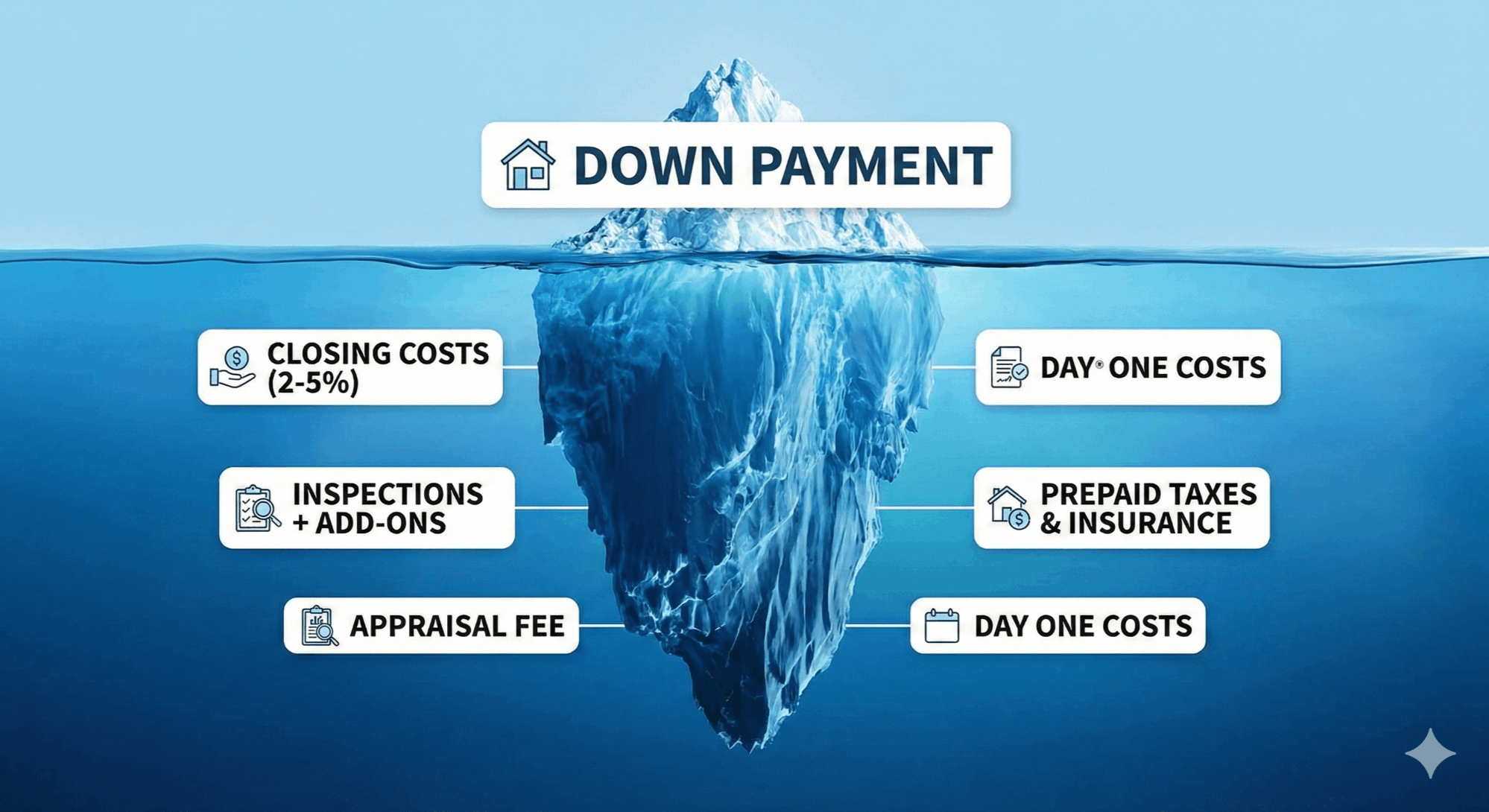

But here is the reality check that many don't get until it's too late: The down payment is just the tip of the iceberg.

If you only budget for the down payment, you are going to find yourself scrambling—and stressed—during the contract period. To ensure a smooth transaction and a happy bank account, you need to know about the "submerged" costs of buying a home.

Here are the five expenses that most often catch first-time buyers by surprise.

1. Closing Costs (The Big One)

While the down payment goes toward the equity in your home, closing costs are the fees required to actually facilitate the transaction. This includes lender origination fees, title insurance, government recording fees, and transfer taxes.

-

The Reality: You need to budget an additional 2% to 5% of the purchase price for closing costs. On a $400,000 home, that’s an extra $8,000 to $20,000 you need to have accessible.

2. The Inspection "Add-Ons"

Most buyers know they need a general home inspection. But a general inspector doesn't look at everything. Depending on the age and location of the home, you may need specialized tests.

-

The Reality: Budget extra for necessary add-ons like Radon testing, Termite/Pest inspections, a Sewer Scope (essential for older homes), or water quality checks for properties on a well.

3. The Appraisal Fee

Before a lender will give you a mortgage, they need to verify the home is actually worth what you offered for it. They hire an independent third-party appraiser to determine the value—and you, the buyer, pay for it.

-

The Reality: This is typically an upfront cost paid during the contract period, usually ranging from $500 to $800.

4. Prepaid Taxes and Insurance

Lenders want to ensure your property taxes and homeowners insurance are paid on time. To do this, they usually require you to pre-pay several months (or even a full year) of these expenses upfront at closing to set up an escrow account.

-

The Reality: This can add thousands to your "cash to close" amount on closing day, depending on your local tax rates.

5. The "Day One" Move-In Costs

You got the keys! Congratulations! Now, how are you getting your couch there?

-

The Reality: Don't forget to budget for the immediate costs of ownership: hiring movers or renting a truck, utility deposit fees, changing the locks on day one, and perhaps buying furniture for rooms you didn't have in your previous rental.

Know the Full Picture Before You Buy

Don't let this list scare you away from homeownership. The goal isn't to panic; the goal is to prepare. Knowing these costs upfront allows you to build a realistic budget so the home-buying process is exciting, not terrifying.

Want a clear picture of what it really costs to buy in our current market? Send me a message, and I’d be happy to walk you through a buyer's cost estimate worksheet.

Categories

Recent Posts